Before we had

An Embedded Flow

A flow that does not allow re-using methods and does

not follow consistent design language

We made

smallcase Checkout

An integrated payment flow that can seamlessly be

used by all use cases on smallcase

Context

Why do we need a Custom Checkout?

For introduction of new products which require multiple gateways, owing to their requirements.

To allow users to save and utilise their preferred methods across the platform.

To improve messaging of essential contextual information related to the payment.

To provide a payment experience consistent with our design language.

Understanding the problem

User Research

Actually...

Here, I will go over specific design problems I had to solve while working on this project. Since payment checkouts are a very common type of user journey, users often have concrete mental models for them.

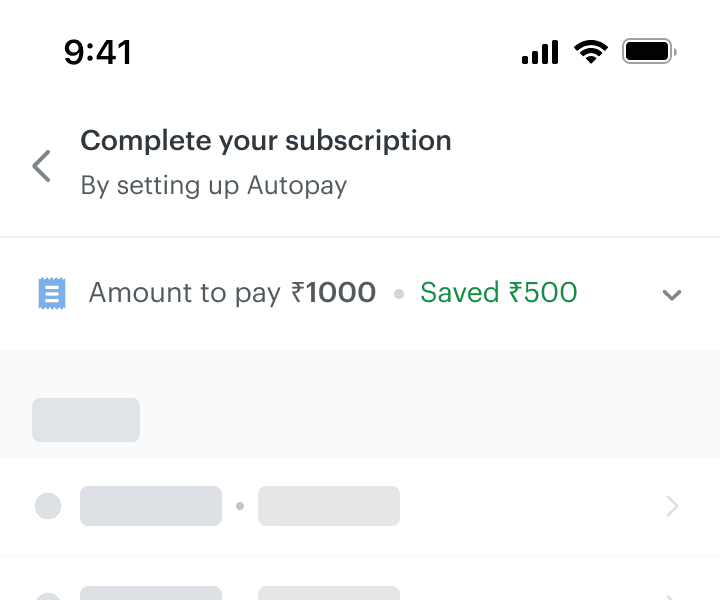

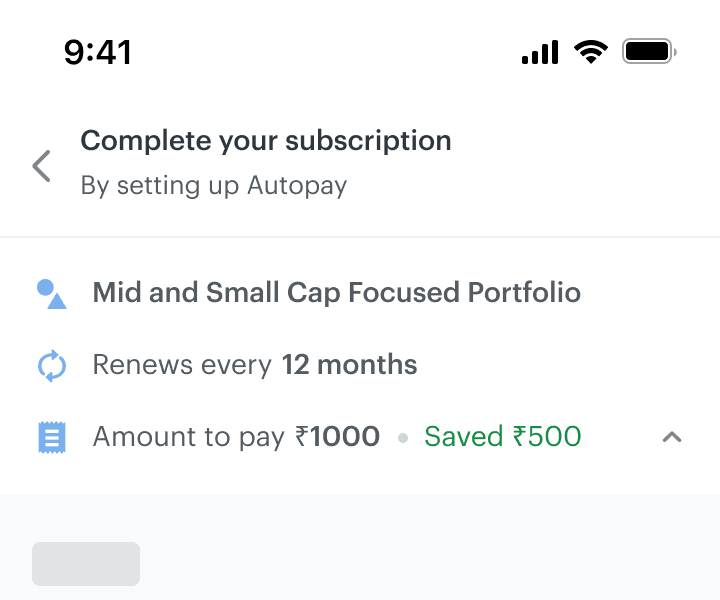

Header & Payment Details

Payment details needed to be customisable to accommodate different payment use cases

The user should be able to find answers to the following questions when they look for payment details:

🤔

How much do I have to pay?

🤔

How was this amount decided?

🤔

Is this a recurring or one time payment?

STEP 1

Designing the component for the primary use case

Final design

Version 1

Version 2

Version 3

Default collapsed view

Expanded view

Simplified amount in he header

Type of payment and the use case for which which it is being made.

Simplified by collapsing details and showing the main data point: Total amount

On expanding, the necessary product details can be seen in a simple manner

STEP 2

Scaling the component to multiple use cases

The expanded Product Details section shows the amount to pay and the rationale behind it’s calculation.

While some use cases (like the one shown above) have conditional rationale attached to the pricing, others have a more arithmetic breakup. To cater to this, I came up with 2 variants of the component:

List format

To be used when the breakdown is conditional. This requires more text-based information using natural-language copy

Example: Subscribing to smallcase

D = (For A, set amount for B) - C

D

Amount to pay

C

Savings from offers

B

Duration of plan

A

Selected smallcase

Table format

Suitable where the amount is calculated based on addition or subtraction of components

Example: Repaying unpaid interest on loan

D = A+B+C

D

C

B

A

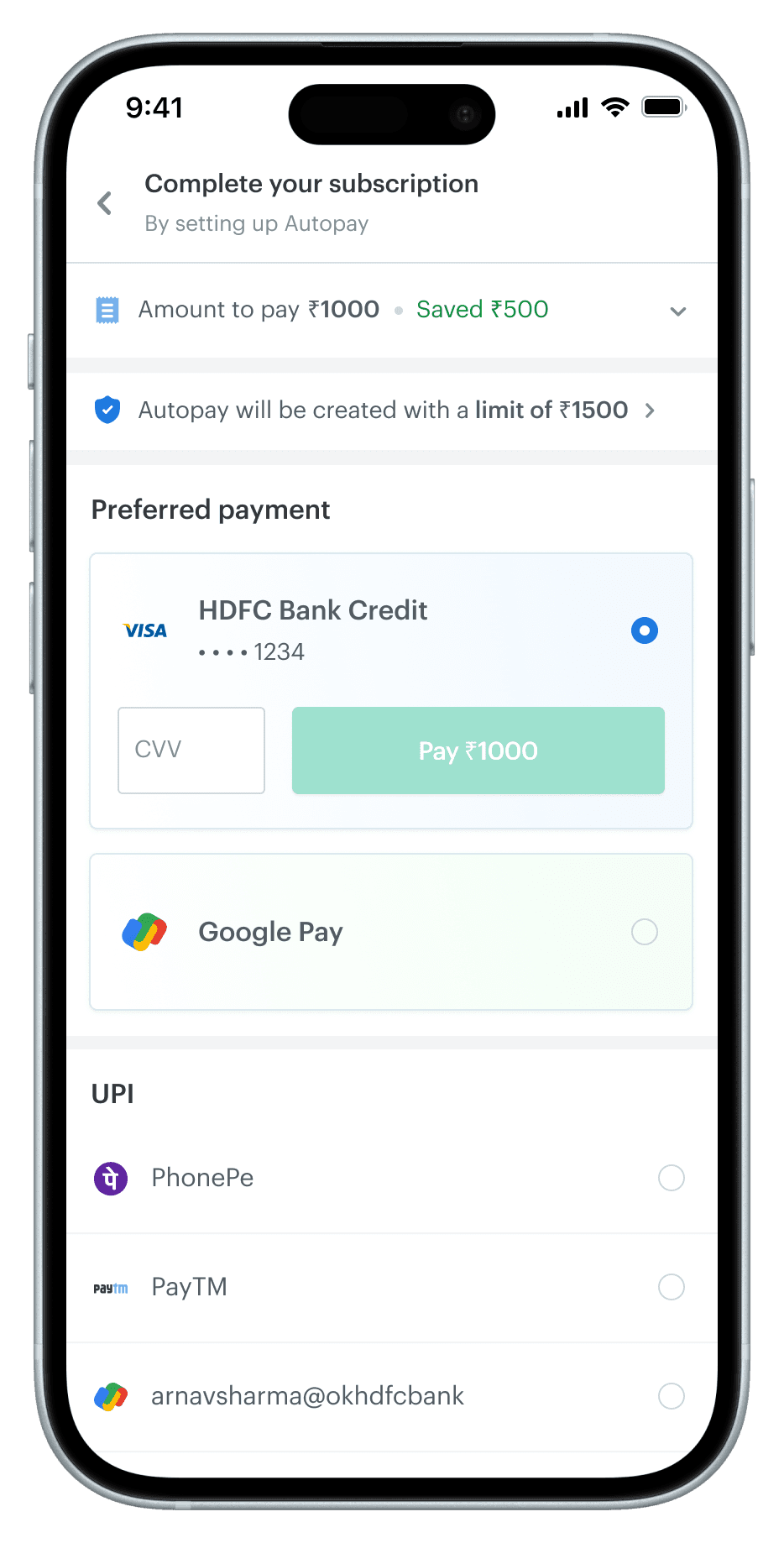

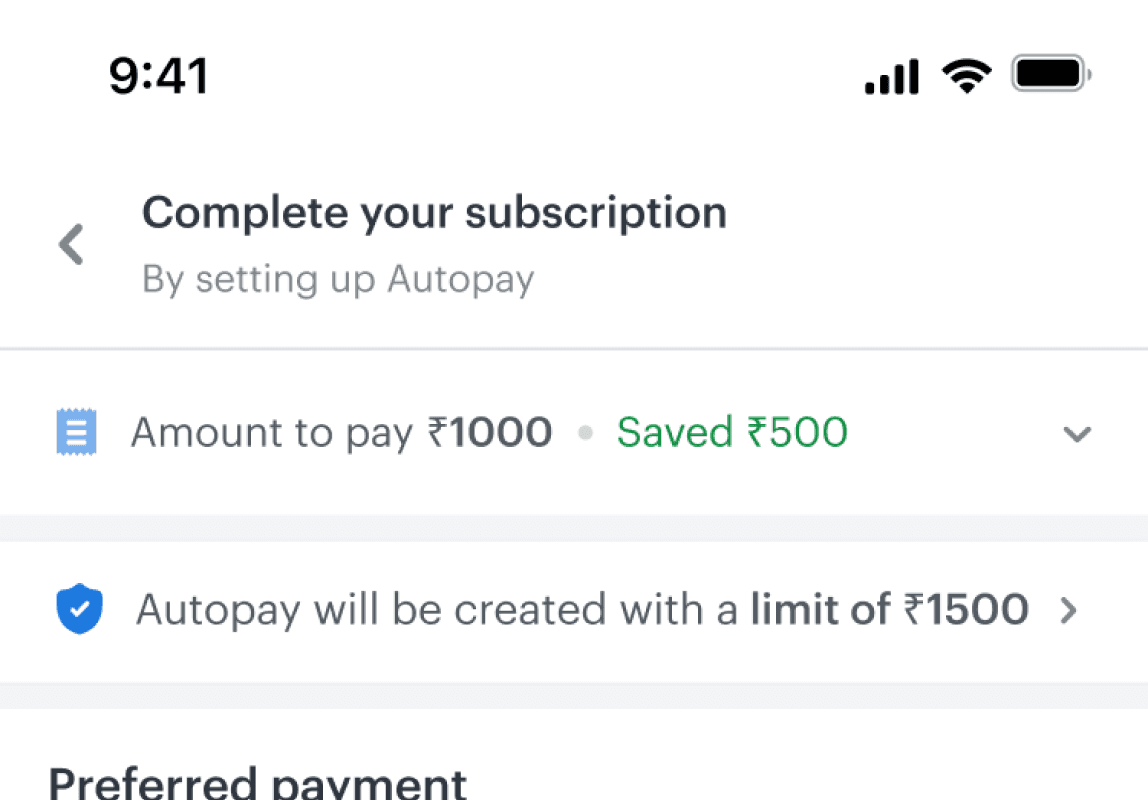

Additional Information bar

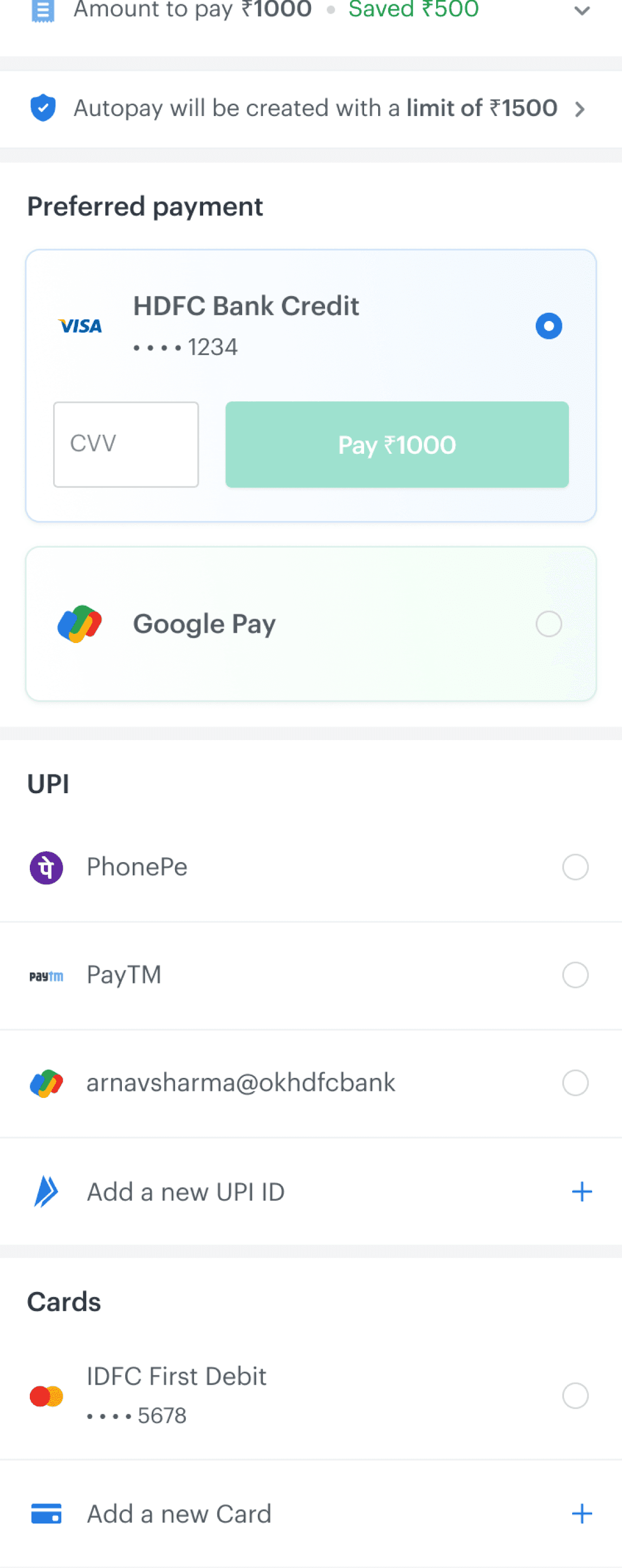

People dropped off because they didn’t know how Autopay Mandates work. We created an info bar to educate them.

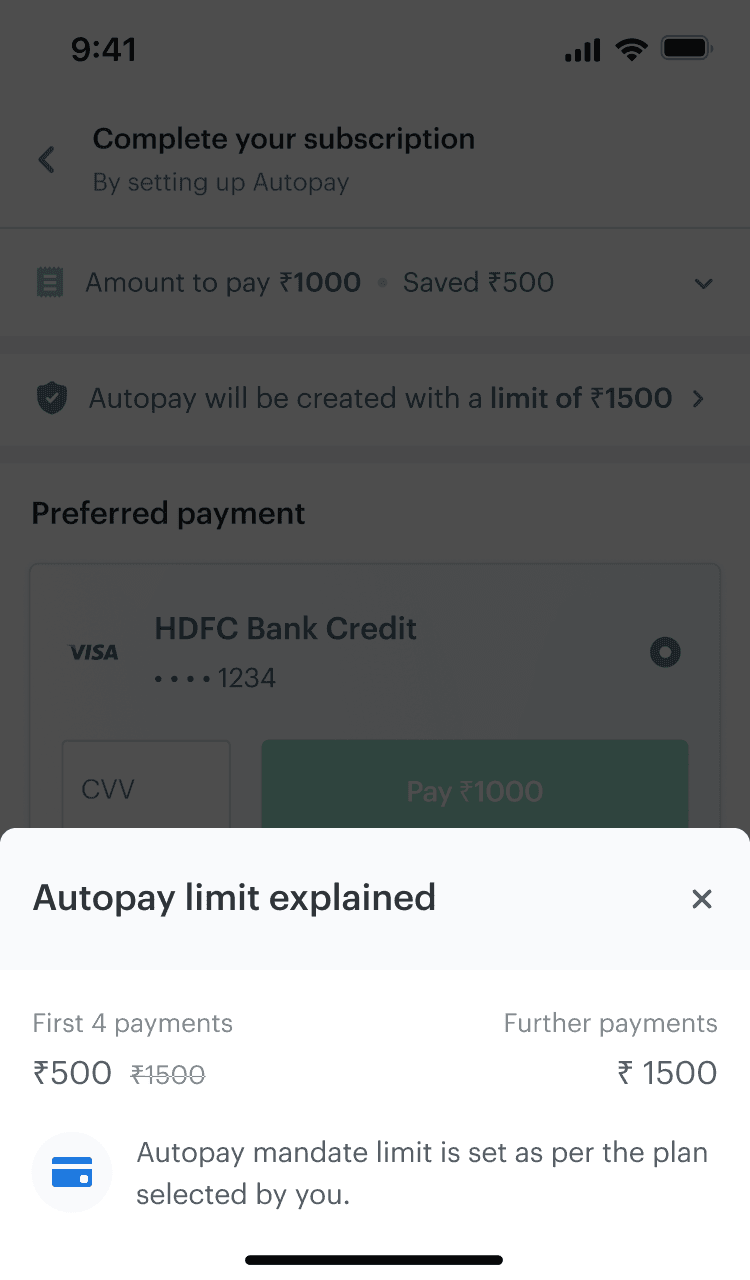

As per security guidelines in India, users are required create Autopay mandates to allow recurring debits.

Each mandates has a maximum limit per debit set as per the full subscription amount.

An issue occurs when the user applies a one-time-only offer coupon on their subscription. Let’s see how:

How Auto-Debits work with Offers

Auto-debit 1

One-time ₹500 offer applied, discounted amount

- ₹ 1000

Auto-debit 2

Offer exhausted, reverted to original plan amount

- ₹ 1500

A user’s journey through subscribing with an offer

Wuhu!

You saved

₹500

Set up

autopay for

₹1500

₹ 1000 was debited by smallcase

🙂

“I’ll go for the ₹1500 plan for this smallcase”

🤩

“Oh wow, I got a ₹500 discount"

😰

“Wait what?! Where did my savings go?”

😮💨

“Oh okay, they only debited ₹1000”

31% users dropped off here

Solving this problem through explicit communication

Final design

Initial ideas

By giving this information it’s own space, we can call out the mismatch before it causes any confusion later.

This bottomsheet explains how once the offer runs out, the user will be charged the full amount, and thus the set limit of the autopay.

Fun fact!

Originally, the company providing the tech for this flow did not have this component readily available. After specially developing it for us, they saw value in it and have started advising other clients to use it for recurring debits 😄

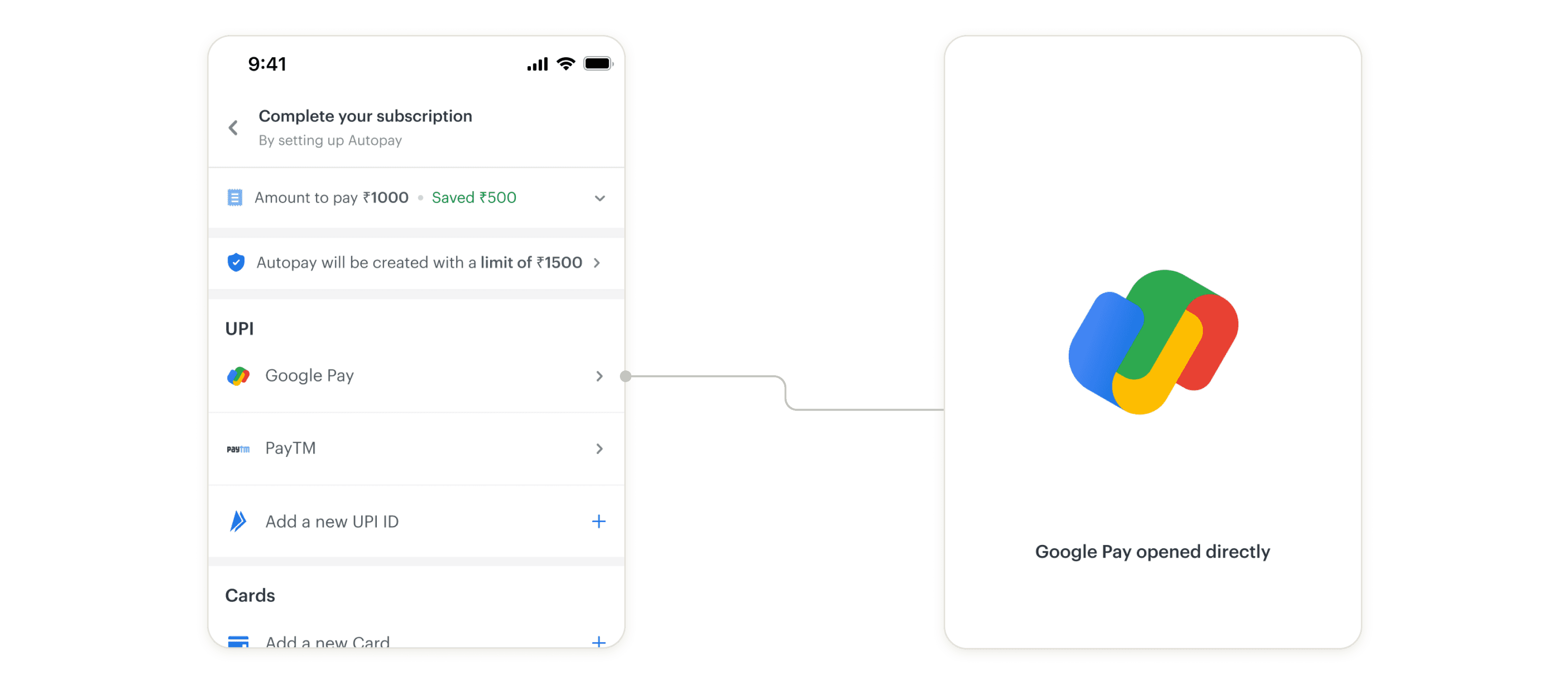

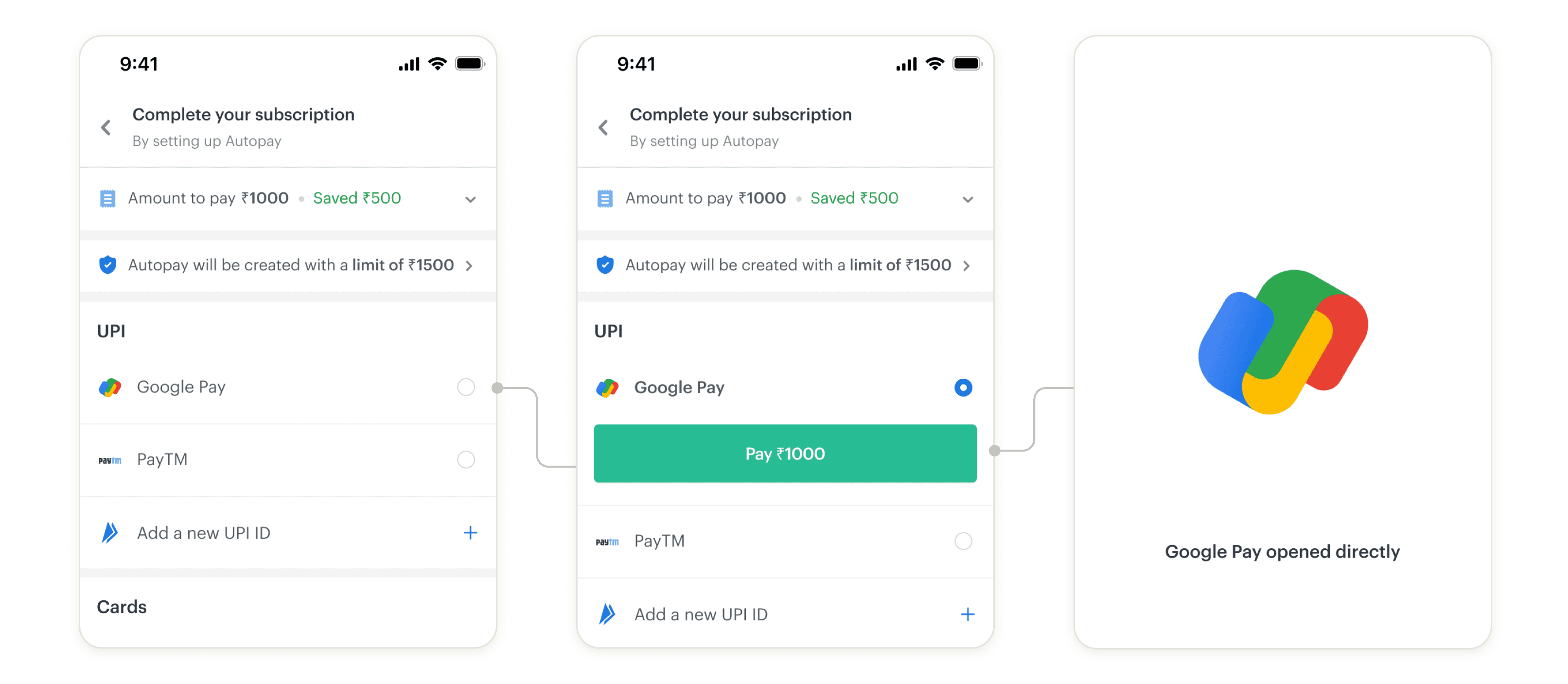

Payment Option Selection

One-click payments are fast but they also lead to more errors. Positive friction is needed.

While designing the payment flows, my basic assumption was “Lesser the clicks, easier the workflow.” Therefore, I initially designed single-click flows for online methods like UPI (Indian version of Zelle).

Version 1

However, we found out that this leads to a significant decrease in success rates as people end up clicking on these options by mistake. So I adjusted the design as follows:

Version 2

This reduces the risk for error as the person selecting the option gets to a second to review their selected option, in turn reducing the need to cancel the transaction to go back.

Preferred Payment

70% payment methods were saved, but were not available to reuse before. Returning UX became very important.

Users could save multiple payment methods, which could increase the decision making time due to increased options on the screen (Hick’s Law).

To tackle this, we have the Preferred Payment section that prioritizes the saved method based on relevance for faster selection.

I went with a card format, to add emphasis on these methods using color and size.

If you decide to save more than 2 methods, the lesser relevant ones are shown as part of the category they belong to.

Payment flows

People are comfortable with existing payment flows. So, we kept it simple and didn’t reinvent the wheel.

Check out (pun intended :P) the full prototype of the entire payment experience in the prototype below:

Results

Payment success rates increased by 21%

This raise can be attributed to the extension of functionality in the payment flow along with a simplified UX. Along with this, it was noted that 36% payments were happening through a saved payment method.